UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For fiscal year ended December 31, 2013

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number 001-10932

WisdomTree Investments, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 13-3487784 | |

| (State or other jurisdiction of incorporation or organization) |

(IRS Employer Identification No.) | |

| 245 Park Avenue, 35th Floor New York, New York |

10167 | |

| (Address of principal executive officers) | (Zip Code) | |

212-801-2080

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: |

Name of each exchange on which registered: | |

| Common Stock, $0.01 par value | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in 12b-2 of the Exchange Act.

| x | Large accelerated filer | ¨ | Accelerated filer | |||||||

| ¨ | Non-accelerated filer (Do not check if a smaller reporting company) | ¨ | Smaller reporting company | |||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

At June 30, 2013, the aggregate market value of the registrant’s Common Stock held by non-affiliates (computed by reference to the closing sale price of such shares on the NASDAQ Global Select Market on June 28, 2013) was $1,166,704,557.

At February 18, 2014, there were 132,699,903 shares of the registrant’s Common Stock outstanding (voting shares).

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this Report, to the extent not set forth herein, is incorporated herein by reference from the registrant’s definitive proxy statement relating to the Annual Meeting of Stockholders to be held in 2014, which definitive proxy statement shall be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this Report relates.

WISDOMTREE INVESTMENTS, INC.

Form 10-K

For the Fiscal Year Ended December 31, 2013

i

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements that are based on our management’s belief and assumptions and on information currently available to our management. Although we believe that the expectations reflected in these forward-looking statements are reasonable, these statements relate to future events or our future financial performance, and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

In some cases, you can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue” or the negative of these terms or other comparable terminology. These statements are only predictions. You should not place undue reliance on forward-looking statements because they involve known and unknown risks, uncertainties and other factors, which are, in some cases, beyond our control and which could materially affect results. Factors that may cause actual results to differ materially from current expectations include, among other things, those listed in the section entitled “Risk Factors” and elsewhere in this Report. If one or more of these risks or uncertainties occur, or if our underlying assumptions prove to be incorrect, actual events or results may vary significantly from those implied or projected by the forward-looking statements. No forward-looking statement is a guarantee of future performance. You should read this Report and the documents that we reference in this Report and have filed with the Securities and Exchange Commission as exhibits to this Report, completely and with the understanding that our actual future results may be materially different from any future results expressed or implied by these forward-looking statements.

In particular, forward-looking statements in this Report include statements about:

| • | anticipated trends, conditions and investor sentiment in the global markets and exchange traded funds (“ETFs”); |

| • | anticipated levels of inflows into and outflows out of our ETFs; |

| • | our ability to deliver favorable rates of return to investors; |

| • | our ability to develop new products and services; |

| • | our ability to maintain current vendors or find new vendors to provide services to us at favorable costs; |

| • | our ability to successfully expand our business into non-U.S. markets; |

| • | competition in our business; and |

| • | the effect of laws and regulations that apply to our business. |

The forward-looking statements in this Report represent our views as of the date of this Report. We anticipate that subsequent events and developments may cause our views to change. However, while we may elect to update these forward-looking statements at some point in the future, we have no current intention of doing so except to the extent required by applicable law. Therefore, these forward-looking statements do not represent our views as of any date other than the date of this Report.

2

| ITEM 1. | BUSINESS |

Our Company

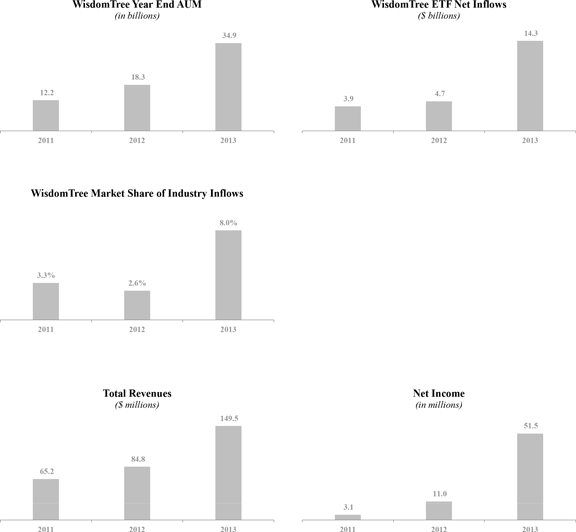

We are the only publicly-traded asset management company that focuses exclusively on ETFs. We are the fifth largest ETF sponsor in the United States with assets under management (“AUM”) of approximately $34.9 billion as of December 31, 2013. Our family of ETFs includes fundamentally weighted funds that track our own indexes, funds that track third party indexes and actively managed funds. We distribute our ETFs through all major channels within the asset management industry, including brokerage firms, registered investment advisers, institutional investors, private wealth managers and discount brokers.

We focus on creating ETFs for investors that offer thoughtful innovation, smart engineering and redefined investing. Most of our index-based funds employ a fundamental weighted investment methodology, which weights securities on the basis of factors such as dividends or earnings, whereas most other ETF industry indexes use a capitalization weighted methodology. In addition, we also offer actively managed ETFs, which are ETFs that are not based on a particular index but rather are actively managed with complete transparency into the ETF’s portfolio on a daily basis. Our regulatory exemptive relief enables us to use our own indexes for certain of our ETFs and actively manage other ETFs.

In evaluating the performance of our Equity, Fixed Income and Alternatives ETFs against actively managed and index based mutual funds and ETFs, as of December 31, 2013 85% of the $33.9 billion invested in our ETFs and 56% (28 of 50) of our Equity, Fixed Income and Alternatives ETFs outperformed their comparable Morningstar average since inception.

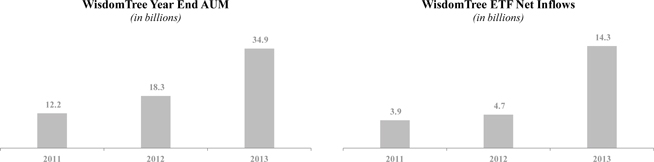

Our AUM has been growing and reaching record levels each year from $12.2 billion at the end of 2011 to $18.3 billion at the end of 2012 and $34.9 billion at the end of 2013. Our net inflows also increased during that time period from $3.9 billion in 2011 to $4.7 billion in 2012 and $14.3 billion in 2013. As a result of strong net inflows and growth in our AUM, our revenues have increased from $65.2 million in 2011 to $84.8 million in 2012 and $149.5 million in 2013 which has helped improve our profitability from a net income of $3.1 million in 2011 to $11.0 million in 2012 and $51.5 million in 2013.

The following charts show our AUM, net inflows, total revenues and net income for the periods indicated:

3

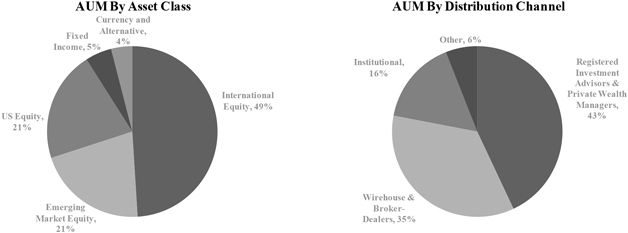

The following charts reflect the asset mix and distribution of our ETFs as of December 31, 2013:

Our Industry

An ETF is an investment fund that holds securities such as equities or bonds and/or other assets such as derivatives or commodities, and that generally trades at approximately the same price as the net asset value of its underlying components over the course of the trading day. ETFs offer exposure to a wide variety of asset classes and investment themes, including domestic, international and global equities, fixed income securities, as well as securities in specific industries and countries. There are also ETFs that track certain specific investments, such as commodities, real estate or currencies.

4

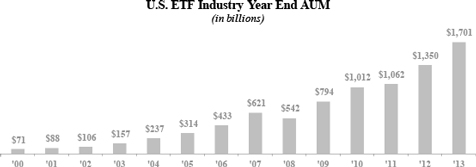

We believe ETFs have been one of the most innovative, revolutionary and disruptive investment products to emerge in the last two decades in the asset management industry. As of December 31, 2013, there were approximately 1,500 ETFs in the United States with aggregate AUM of $1.7 trillion. BlackRock, Inc. projects the U.S. aggregate AUM of ETFs could grow to $3.5 trillion by 2017. The chart below reflects the AUM of the ETF industry in the United States since 2000:

Source: BlackRock

As of December 31, 2013, we were the fifth largest ETF sponsor in the United States by AUM and had the second highest percentage growth rate in AUM of the top ten ETF sponsors at the end of 2013:

| AUM as of (in billions)(1) |

2013 % Organic Growth in AUM (2) | |||||||||||

| 1 |

iShares | $ | 662 | 7.3 | % | |||||||

| 2 |

State Street | 376 | 4.5 | % | ||||||||

| 3 |

Vanguard | 334 | 22.7 | % | ||||||||

| 4 |

PowerShares | 97 | 34.9 | % | ||||||||

|

5 |

WisdomTree | 35 | 78.5 | % | ||||||||

| 6 |

ProShares | 27 | 31.9 | % | ||||||||

| 7 |

Van Eck | 22 | 5.6 | % | ||||||||

| 8 |

Guggenheim | 22 | 58.1 | % | ||||||||

| 9 |

First Trust | 20 | 99.8 | % | ||||||||

| 10 |

Schwab | 17 | 71.5 | % | ||||||||

|

|

|

|||||||||||

| Top Ten Total | 1,612 | |||||||||||

|

|

|

|||||||||||

| Other U.S. ETF Sponsors | 89 | |||||||||||

|

|

|

|||||||||||

| Total U.S. ETF Industry AUM | $ | 1,701 | ||||||||||

|

|

|

|||||||||||

| (1) | Source: BlackRock |

| (2) | Source: Strategic Insight |

According to Morningstar, Inc., ETFs were initially marketed primarily to institutional investors. However, today, institutional investors account for only about half of the assets held in ETFs. ETFs have become more popular among a broad range of investors as they come to understand their benefits and use them for a variety of purposes and strategies, including low cost index investing and asset allocation, access to specific asset classes, protective hedging, income generation, exploitation of arbitrage opportunities, and diversification strategies.

5

While ETFs are similar to mutual funds in many respects, they have some important differences as well:

| • | Transparency. ETFs disclose the composition of their underlying portfolios on a daily basis, unlike mutual funds which typically disclose their holdings only every 90 days. |

| • | Intraday trading, hedging strategies and complex orders. Like stocks, ETFs can be bought and sold on exchanges throughout the trading day at market prices. ETFs update the indicative values of their underlying portfolios every 15 seconds. As publicly-traded securities, ETF shares can be purchased on margin and sold short, enabling the use of hedging strategies, and traded using stop orders and limit orders, which allow investors to specify the price points at which they are willing to trade. |

| • | Tax efficiency. In the United States, whenever a mutual fund or ETF realizes a capital gain that is not balanced by a realized loss, it must distribute the capital gain to its shareholders. These gains are taxable to all shareholders, even those who reinvest the gain distributions in additional shares of the fund. However, most ETFs typically redeem their shares through “in-kind” redemptions in which low-cost securities are transferred out of the ETF in exchange for fund shares in a non-taxable transaction. As a practical matter, mutual funds cannot use this process. By using this process, ETFs avoid the transaction fees and tax impact incurred by mutual funds that sell securities to generate cash to pay out redemptions. |

| • | Uniform pricing. From a cost perspective, ETFs are one of the most equitable investment products on the market. Investors, regardless of their size, structure or sophistication, pay identical advisory fees. Unlike mutual funds, ETFs do not have different share classes or different expense structures for retail and institutional clients and ETFs are not sold with sales loads or 12b-1 fees. In many cases, ETFs offer lower expense ratios than comparable mutual funds. |

ETFs are used in various ways by a range of investors, from conservative to speculative uses including:

| • | Low cost index investing. ETFs provide exposure to a variety of broad-based indexes across equities, commodities, fixed income, and other asset classes and strategies, and can be used as both long-term portfolio holdings or short term trading tools. ETFs offer an efficient and less costly method by which to gain exposure to indexes as compared to individual stock ownership. |

| • | Improved access to specific asset classes. Investors often use ETFs to gain access to specific market sectors or regions around the world by investing in an ETF that holds a portfolio of securities in that region or segment rather than buying individual securities. |

| • | Protective hedging. Investors seeking to protect their portfolios may use ETFs as a hedge against unexpected declines in prices. |

| • | Income generation. Investors seeking to obtain income from their portfolios may buy dividend-paying ETFs, which encompass a basket of dividend-paying stocks rather than buying individual stocks or a fixed income ETF that typically distributes monthly income. |

| • | Speculative investing. Investors with a specific directional opinion about a market sector may choose to buy or sell (long or short) an ETF covering or leveraging that market sector. |

| • | Arbitrage. Sophisticated investors may use ETFs in order to exploit perceived value differences between the ETF and the value of the ETF’s underlying portfolio of securities. |

| • | Asset allocation. Investors seeking to invest in various asset classes to develop an asset allocation model in a cost-effective manner can do so easily with ETFs, which offer broad exposure to various asset classes in a single security. |

| • | Diversification. By definition, ETFs represent a basket of securities and each fund may contain hundreds or even thousands of different individual securities. The “instant diversification” of ETFs provides investors with broad exposure to an asset class, market sector or geography. |

6

ETFs are one of the fastest growing sectors of the asset management industry, having expanded from $66 billion in AUM at the beginning of 2000 to $1.7 trillion in AUM at the end of 2013. According to the Investment Company Institute, since 2007 ETFs have generated approximately 51% of the total inflows into ETFs and long-term mutual funds. However, during that time ETFs generated positive inflows into equity funds of approximately $821 billion and long-term equity mutual funds experienced outflows of approximately $298 billion. We believe this trend is due to the inherent benefits of ETFs, that is: transparency, liquidity and tax efficiency.

We believe our growth, and the growth of the ETF industry in general, will continue to be driven by the following factors:

| • | Education and greater investor awareness. Over the last several years, ETFs have been taking a greater share of inflows and AUM from mutual funds. We believe as a result of market downturns, during the economic crisis investors have become more aware of some of the deficiencies of mutual funds and other financial products. In particular, we believe investors are beginning to focus on important characteristics of their traditional investments—namely transparency, tradability, liquidity, tax efficiency and fees. Their attention and education focused on these important investment characteristics may be one of the drivers of the shift in inflows from traditional mutual funds to ETFs. We believe as investors become more aware and educated about ETFs and their benefits, ETFs will continue to take market share from traditional mutual funds and other financial products or structures such as hedge funds, separate accounts and individual stocks. |

| • | Move to fee-based models. Over the last several years, many financial advisers have changed the revenue model that they charge clients from one that is “transaction-based,” that is, based on commissions for trades or receiving sales loads, to a “fee-based” approach, where an overall fee is charged based on the value of AUM. This fee-based approach lends itself to the adviser selecting no-load, lower-fee financial products, and in our opinion, better aligns advisers with the interests of their clients. Since ETFs generally charge lower fees than mutual funds, we believe this model shift will benefit the ETF industry. As major brokerage firms and asset managers encourage their advisers to move towards fee-based models, we believe overall usage of ETFs will likely increase. |

| • | Innovative product offerings. Historically, ETFs tracked traditional equity indexes, but the volume of ETF growth has led to significant innovation and product development. As demand increased, the number of ETFs has also increased and today, ETFs are available for virtually every asset class including commodities, fixed income, alternative strategies, leveraged/inverse, real estate and currencies. We believe, though, that there remain substantial areas for ETF sponsors to continue to innovate, including alternative-and investment theme-based strategies, hard and soft commodities, and actively-managed strategies. We believe the further expansion of ETFs will fuel further growth and investments from investors who typically access these products through hedge funds, separate accounts, stock investments or the futures and commodity markets. |

| • | New distribution channels. Discount brokers, including E*Trade, TD Ameritrade, Schwab and Fidelity, now offer free trading and promotion of select ETFs. We believe the promotion of ETF trading by discount brokers and their marketing of ETFs to a wider retail channel will contribute to the future growth of ETFs. |

| • | Changing demographics. As the “baby boomer” generation continues to mature and retire, we expect that there will be a greater demand for a broad range of investment solutions, with a particular emphasis on income generation and principal protection, and that more of these investors will seek advice from professional financial advisers. We believe these financial advisers will migrate more of their clients’ portfolios to ETFs due to their lower fees, better fit within fee-based models, and their ability to (i) provide access to more diverse market sectors, (ii) improve multi-asset class allocation, and (iii) be used for different investment strategies, including income generation. Overall, we believe ETFs are well-suited to meet the needs of this large and important group of investors. In addition, since many younger investors and financial advisers have demonstrated a preference for the ETF structure over traditional product structures, we believe that wealth transfers from one generation to another will also have a positive effect on ETF industry growth. |

7

| • | Expansion into 401(k) retirement plans. Historically, 401(k) plans were almost exclusively comprised of mutual funds. However, we believe ETFs are particularly well-suited to 401(k) retirement plans and that these plans present a large and growing opportunity for our industry. ETFs are easy-to-implement, fully transparent investment vehicles covering the full range of asset allocation categories, and are available at significantly lower costs than most traditional mutual funds. In addition, regulatory reform laws which recently went into effect require 401(k) retirement plan sponsors to disclose all fees associated with their plans. While it may take several years for the fee disclosures to be fully analyzed and understood by plan sponsors and their participants, we believe that as investors become aware of fees associated with using mutual funds in traditional 401(k) retirement plans, they will replace higher fee mutual funds with ETFs because of their lower fees. |

| • | International Markets. We believe the growth of ETFs is a global phenomenon. While the U.S. currently represents the vast majority of global ETF assets, Europe, Asia and Latin America are growing quickly. The same growth drivers powering the U.S. ETF industry are gradually taking hold in global markets. Additionally, there is an increasing trend of non-U.S. institutional investors investing in U.S.-listed ETFs. |

Our Competitive Strengths

| • | Well-positioned in large and growing markets. We believe that ETFs are well-positioned to grow significantly faster than the asset management industry as a whole, making our concentration in ETFs a significant advantage versus other traditional asset management firms. In 2011, 2012, and 2013, our AUM grew among the fastest rate of the top 10 ETF sponsors and at December 31, 2013 we were the fifth largest ETF sponsor in the United States by AUM. Within the ETF industry, being a first mover, or one of the first providers of ETFs in a particular asset class, can be a significant advantage. We believe that our early leadership in a number of asset classes positions us well to maintain a leadership position. |

| • | Strong performance. We create our own indexes, rebalanced annually, most of which weight companies in our equity ETFs by a measure of fundamental value. In contrast, traditional indexes are market capitalization weighted and tend to track the momentum of the market. In addition, we also offer actively managed ETFs, which are ETFs that are not based on a particular index but rather are actively managed with complete transparency into the ETF’s portfolio on a daily basis, as well as ETFs based on third party indexes. In evaluating the performance of our Equity, Fixed Income and Alternatives ETFs against actively managed and index based mutual funds and ETFs, as of December 31, 2013 85% of the $33.9 billion invested in our Equity, Fixed Income and Alternatives ETFs and 56% (28 of 50) of our ETFs outperformed their comparable Morningstar average since inception. |

| • | Diversified product set, powered by innovation. We have a broad and diverse product set. Our products span a variety of traditional and high growth asset classes, including emerging markets, international and U.S. equities, international and U.S. fixed income, currencies, and alternatives, and include both passive and actively managed funds. Our product development, research and sales teams work closely to identify potential new ETFs for the marketplace. Because we have the regulatory exemptive relief that enables us to use our own indexes for our ETFs, we have the ability to create certain indexes and related ETFs more rapidly than many of our competitors who must license indexes from third party index providers. Our exemptive relief also enables us to offer actively managed funds. Our innovations include launching the industry’s first emerging markets small-cap equity ETF, the first actively managed currency ETFs, one of the first international local currency denominated fixed income ETFs and the first managed futures strategy ETF. We believe that our expertise in product development combined with our regulatory exemptive relief provides a strategic advantage, enabling us to launch innovative ETFs that others may not be able to launch as quickly. |

| • | Extensive marketing, research and sales efforts. We have invested significant resources to establish the WisdomTree brand through targeted television, print and online advertising, social media, as well as through our public relations efforts. The majority of our employees are dedicated to marketing, research and sales. Our sales professionals are the primary points of contact for financial advisers, independent advisory firms and institutional investors who use our ETFs. Their efforts are enhanced through value-added services provided by our research and marketing efforts. We have strong |

8

| relationships with financial advisers at leading national brokerage firms, registered investment advisers and high net worth advisers. We believe the recent growth we have experienced by strategically aligning these adviser relationships and marketing campaigns with targeted research and sales initiatives differentiates us from our competitors and contributes to our strong inflows. |

| • | Efficient business model with lower risk profile. We have invested heavily in the internal development of our core competencies with respect to product development, marketing, research and sales of ETFs. We outsource to third parties those services that are not our core competencies or may be resource or risk intensive, such as the portfolio management responsibilities and fund accounting operations of our ETFs. In addition, since we create our own indexes for most of our ETFs, we usually do not incur licensing costs and can therefore be more competitive in terms of the fees we charge for our index-based ETFs. We have already made substantial investments in our core competencies, and we expect to be able to leverage these existing capabilities across our business, positioning us to maintain both growth and profitability. |

| • | Strong, seasoned and creative management team. We have built a strong and dedicated senior leadership team. Most of our leadership team has significant ETF or financial services industry experience in fund operations, regulatory and compliance oversight, product development and management or marketing and communications. We believe our team, by developing an ETF sponsor from the ground up despite significant competitive, regulatory and operational barriers, has demonstrated an ability to innovate as well as recognize and respond to market opportunities and effectively execute our strategy. |

Our Growth Strategies

Our goal is to become an asset manager with at least $100 billion in ETF AUM, since we believe economies of scale is a competitive advantage in the ETF industry. In 2009, we were the eleventh largest ETF sponsor. We increased our AUM to become the eighth largest ETF sponsor in 2010, the seventh largest in 2012 and the fifth largest in 2013, with $34.9 billion in AUM. We believe our continued execution will enable us to increase trading volumes and build longer performance track records, which should allow us to attract additional investors and, in turn, further grow our AUM. We will seek to increase our market share and build additional scale by continuing to implement the following growth strategies:

| • | Increase penetration within existing distribution channels. We believe there is an opportunity to increase our market share by further penetrating existing distribution channels and by cross-selling additional WisdomTree ETFs. In order to achieve these objectives, we intend to continue our strategy of targeted advertising and direct marketing, coupled with our research-focused sales support initiatives, to enhance product awareness and increase our market share of ETF net inflows. Our share of ETF industry net inflows has fluctuated from 2.7% in 2010, to 3.3% in 2011, to 2.6% in 2012 and 8.0% in 2013. |

| • | Launch innovative new products that diversify our product offerings and revenues. We believe our track record has shown that we can create and sell innovative ETFs that meet market demand. We believe that continued launches of new products will strengthen our business by allowing us to realize additional inflows, maintain and grow our AUM and generate revenues across different market cycles as particular investment strategies move in and out of favor. |

| • | Expand internationally. To date, our sales and marketing has been principally focused on the domestic U.S. market. However, 22 of our ETFs have been cross-listed in the special international section on the Mexican stock exchange, where certain institutional investors trade foreign securities in Mexico. Additionally, 13 of our ETFs were approved by the Chilean pension funds investment regulator for sale to Chilean pension funds and 12 of our ETFs were approved by the Peruvian pension funds investment regulator for sale to Peruvian pension funds. In 2010 we entered into a marketing arrangement with the Compass Group to market WisdomTree ETFs in Latin America. We also filed notifications with the Financial Services Agency of Japan making seven of our ETFs available for sale in Japan through Japanese securities companies. As ETFs are increasingly traded globally, we believe that international expansion of our marketing, communication and sales strategies will provide significant new growth avenues. We have established an Irish Undertakings for Collective Investments in Transferable Securities (“UCITS”) trust to give us the option to capitalize on growth opportunities outside of the United States. On January 31, 2014, we announced a plan to launch a platform for European ETF operations through a majority investment in U.K.-based exchange traded product (“ETP”) provider Boost ETP LLP (“Boost”). Through this platform, we intend to launch a select range of UCITS ETFs under the WisdomTree brand and continue to manage and |

9

| grow the Boost lineup of short and leveraged fully collateralized ETPs under the Boost brand. Subject to regulatory approval and other customary closing conditions, the transaction is expected to close in the first half of 2014. |

| • | Selectively pursue acquisitions or partnerships. We may pursue acquisitions or enter into partnerships or other commercial arrangements that will enable us to strengthen our current business, expand and diversify our product offering, increase our AUM or enter into new markets. We believe entering into partnerships or pursuing acquisitions is a cost-effective means of growing our business and AUM. For example, in 2007, we purchased certain assets and intellectual property from Treasury Equity, LLC which formed the basis for our currency ETFs. In 2008, we entered into a joint venture with Mellon Capital Management Corporation (“Mellon Capital”) and The Dreyfus Corporation (“Dreyfus”) with respect to our currency and fixed income ETFs, which enabled us to bring these ETFs to market faster than would otherwise have been possible. This joint venture ended at the end of 2012. On January 31, 2014 we announced a plan to launch a platform for European ETF operations through a majority investment in Boost described above. |

Regulatory Framework of the ETF Industry

Not all ETPs are ETFs. ETFs are a distinct type of security with features that are different than other ETPs. ETFs are open-end investment companies or unit investment trusts regulated by the Investment Company Act of 1940 (“Investment Company Act”). This regulatory structure is designed to provide investor protection within a pooled investment product. For example, the Investment Company Act requires that at least 40% of the Trustees for each ETF must not be affiliated persons of the fund’s investment manager (“Independent Trustees”). If the ETF seeks to rely on certain rules under the Investment Company Act, a majority of the Trustees for that ETF must be Independent Trustees. In addition, as discussed below, ETFs have received orders from the staff of the SEC which exempt them from certain provisions of the Investment Company Act; however, ETFs generally operate under regulations that prohibit affiliated transactions, are subject to standard pricing and valuation rules and have mandated compliance programs. ETPs can take a number of forms other than ETFs, including exchange traded notes, grantor trusts or limited partnerships. In the U.S. market, a key factor differentiating ETFs, grantor trusts and limited partnerships from exchange traded notes is that the former hold assets underlying the ETP. Exchange traded notes, on the other hand, are debt instruments issued by the exchange traded note sponsor. Also, each of these structures has implications for taxes, liquidity, tracking error and credit risk.

Because ETFs do not fit into the regulatory provisions governing mutual funds, ETF sponsors need to obtain “exemptive relief” from the Securities and Exchange Commission (“SEC”) from certain provisions of the Investment Company Act in order to operate ETFs. This exemptive relief allows the ETF sponsor to bring to market the specific products or structures for which the relief was requested and obtained. Applying for exemptive relief can be costly and take several months to several years depending on the type of exemptive relief sought. See “Business—Regulation” below.

Our Products

As of December 31, 2013, we offered a comprehensive family of 61 ETFs, of which 44 are listed on NYSE Arca, a listing venue of NYSE Euronext, and 17 are listed on the NASDAQ Stock Market. 22 of our ETFs have also been cross-listed on the Mexican stock exchange.

The type and AUM for each of our ETFs as of December 31, 2013:

| Category |

Number of Funds | AUM ($ in Billions) | ||||||

| International Hedged Equity |

6 | 13,348 | ||||||

| Emerging Markets Equity |

7 | 7,448 | ||||||

| U.S. Equity |

13 | 7,181 | ||||||

| International Developed Equity |

16 | 3,864 | ||||||

| Fixed Income |

11 | 1,906 | ||||||

| Currency |

6 | 979 | ||||||

| Alternative Strategy |

2 | 158 | ||||||

|

|

|

|

|

|||||

| Total |

61 | $ | 34,884 | |||||

10

Equity ETFs

We offer equity ETFs that offer access to the securities of large, mid and small-cap companies located in the United States, international developed markets and emerging markets, as well as particular market sectors and styles. Our equity ETFs track our own fundamentally weighted indexes, as opposed to market capitalization weighted indexes, which assign more weight to stocks with the highest market capitalizations. These fundamentally weighted indexes focus on securities of companies that pay regular cash dividends or on securities of companies that have generated positive cumulative earnings over a certain period. We believe weighting equity markets by income, rather than by market capitalization, can provide investors with better risk-adjusted returns over longer term periods in core equity exposures. Our equity ETFs are sub-advised by Mellon Capital, a subsidiary of The Bank of New York Mellon Corporation (“BNY Mellon”).

International Hedged Equity ETFs

In December 2009, we began launching currency hedged equity ETFs and have six such ETFs in the market today. These ETFs provide exposure to a specified international equity market while hedging the currency exposure of that market relative to the U.S. dollar. Our International Hedged Equity ETFs are sub-advised by Mellon Capital.

Currency ETFs

We launched the industry’s first currency ETFs in May 2008 using our regulatory exemption for actively managed funds. We offer currency ETFs that provide investors with exposure to developed and emerging markets currencies, including the Chinese Yuan and the Brazilian Real. In December 2013, we launched a U.S. Dollar Bullish Fund licensing a new Bloomberg index. Currency ETFs invest in U.S. money market securities, forward currency contracts and swaps and seek to achieve the total returns reflective of both money market rates in selected countries available to foreign investors and changes to the value of these currencies relative to the U.S. dollar. Our Currency ETFs are sub-advised by Mellon Capital.

Fixed Income ETFs

In 2010, we began launching international fixed income ETFs that invest in emerging market countries, Asia Pacific ex-Japan countries or European countries. These ETFs are denominated in either local or U.S. currencies. We intend to launch additional fixed income bond funds and broaden our product offerings in this category. Our fixed income ETFs are sub-advised by either Mellon Capital or Western Asset Management, a subsidiary of Legg Mason. In December 2013, we launched a suite of Rising Rate Bond ETFs based on leading fixed income benchmarks we license from third parties. Our Rising Rate Bond ETFs are sub-advised by Mellon Capital.

Alternative Strategy ETFs

In 2011, we launched the industry’s first managed futures strategy ETF and a global real return ETF. We also intend to explore additional alternative strategy products in the future. Our Managed Futures Strategy ETF is sub-advised by Mellon Capital and our Global Real Return ETF is sub-advised by Western Asset Management.

Sales, Marketing and Research

We distribute our ETFs through all major channels within the asset management industry, including brokerage firms, registered investment advisers, institutional investors, private wealth managers and discount brokers. Our primary sales efforts are not directed towards the retail segment but rather are directed towards the financial or investment adviser who acts as the intermediary between the end-client and us. We do not pay commissions nor do we offer 12b-1 fees to financial advisers to use or recommend the use of our ETFs.

We have developed an extensive network and relationships with financial advisers and we believe our ETFs and related research are well structured to meet their needs and those of their clients. Our sales professionals act in a consultative role to provide the financial adviser with value-added services. We seek to consistently grow our network of financial advisers and we opportunistically seek to introduce new products that best deliver our investment strategies to investors through these distribution channels. We have our own team of 40 sales professionals located in the United States as of December 31, 2013.

11

In addition, we have agreements with third parties to serve as the external marketing agents for the WisdomTree ETFs in Latin America as well as with E*Trade Financial to allow our ETFs to trade commission free on its brokerage platform in exchange for a percentage of our advisory fee revenue from certain AUM. We believe these arrangements expand our distribution capabilities in a cost-effective manner and we may continue to enter into such arrangements in the future.

Our marketing effort is focused on three objectives: (i) generating new clients and inflows to our ETFs; (ii) retaining existing clients, with a focus on cross-selling additional WisdomTree ETFs; and (iii) building brand awareness. We pursue these objectives through a multi-faceted marketing strategy targeted at financial advisers. We utilize the following strategies:

| • | Targeted advertising. We create highly targeted multi-media advertising campaigns limited to established core financial media. For example, our television advertising runs exclusively on the cable networks CNBC and Bloomberg Television; online advertising runs on investing or ETF-specific web sites, such as www.seekingalpha.com and www.etfdatabase.com; and print advertising runs in core financial publications, including Barron’s and Investor’s Business Daily. |

| • | Media relations. We have a full time public relations team who have established relationships with the major financial media outlets including: the Wall Street Journal, Barron’s, the Financial Times, Bloomberg, Reuters and USA Today. We utilize these relationships to help create awareness of the WisdomTree ETFs and the ETF industry in general. Several members of our management team are frequent market commentators and conference panelists. |

| • | Direct marketing. We have a database of financial advisers to which we regularly market through targeted and segmented communications, such as on-demand research presentations, ETF-specific or educational events and presentations, quarterly newsletters and market commentary from our senior investment strategy adviser, Professor Jeremy Siegel. |

| • | Social media. We have implemented a social media strategy that allows us to connect directly with financial advisers and investors by offering timely access to our research material and more general market commentary. Our social media strategy allows us to continue to enhance our brand reputation of expertise and thought leadership in the ETF industry. |

| • | Sales support. We create comprehensive materials to support our sales process including whitepapers, research reports, webinars, blogs, podcasts and performance data for our ETFs. |

We will continue to evolve our marketing and communication efforts in response to changes in the ETF industry, market conditions and marketing trends.

Our research team has three core functions: index development and oversight, investment research and sales support. In its index development role, the research group is responsible for creating the investment methodologies and overseeing the maintenance of our indexes that WisdomTree’s equity ETFs are designed to track. The team also provides a variety of investment research around these indexes and market segments. Our research is typically academic-type research to support our products, including white papers on the strategies underlying our indexes and ETFs, investment insights on current market trends, and types of investment strategies that drive long-term performance. We distribute our research through our sales professionals, online through our website and blog, targeted emails to financial advisers, or through financial media outlets. On some occasions our research has been included in “op-ed” articles appearing in the Wall Street Journal. Shorter research notes are also developed to promote our ideas which are distributed online through social media channels. Finally, the research team supports our sales professionals in meetings as market experts and through custom analysis on client portfolio holdings. In addition, we consult with our senior investment strategy adviser, Professor Jeremy Siegel, on product development ideas and market commentaries.

Product Development

We are focused on driving continued growth through innovative product development. Due to our broad based regulatory exemptive relief, proprietary index development capabilities, and a strategic focus on product development at the senior management level, we have demonstrated an ability to launch innovative and differentiated ETFs. When developing new funds, we seek to introduce product that can be first to market, offer some improvement in structure or strategy relative to an incumbent product, or offer some other key distinction relative to an incumbent product. In short, we want to add choice in the market and seek to introduce thoughtful investment solutions by avoiding commoditized product. Lastly, when launching new products we seek to expand and diversify our overall product line.

12

Competition

The asset management industry is highly competitive and we face substantial competition in virtually all aspects of our business. Factors affecting our business include fees for our products, investment performance, brand recognition, business reputation, quality of service and the continuity of our financial adviser relationships. We compete directly with other ETF sponsors and mutual fund companies and indirectly against other investment management firms, insurance companies, banks, brokerage firms and other financial institutions that offer products that have similar features and investment objectives to those offered by us. The vast majority of the firms we compete with are subsidiaries of large diversified financial companies and many others are much larger in terms of AUM, years in operations and revenues and, accordingly, have much larger sales organizations and budgets. In addition, these larger competitors may attract business through means that are not available to us, including retail bank offices, investment banking, insurance agencies and broker-dealers.

The ETF industry is becoming significantly more competitive as existing players compete on price and broaden their suite of products to different strategies, in some cases, similar to ours. For example, in August 2013, Charles Schwab & Co. launched six ETFs using the Russell fundamentally weighted indexes with fees generally equivalent with our comparable ETFs. In September 2013, iShares filed a registration statement for three currency hedged equity ETFs including a Japan hedged equity ETF. Those ETFs launched in February 2014 with fees generally equivalent with comparable ETFs. Also, Deutsche Bank renamed five of their equity ETFs to stress their currency hedging strategy and launched three additional currency hedged equity ETFs. More recently, iShares launched a floating rate treasury ETF on the same day as we launched our similar ETF; however, iShares waived fees for one year while we did not.

We do not know what effect, if any, the launch of these ETFs may have on our business. Within the ETF industry, being a first mover, or one of the first providers of ETFs in a particular asset class, can be a significant advantage, as the first ETF in a category to attract scale in AUM and trading liquidity is generally viewed as the most attractive ETF. We believe that our early launch of ETFs in a number of asset classes or strategies, including fundamental weighting and currency hedging, positions us well to maintain our position as one of the leaders of the ETF industry.

In 2008, the SEC announced a proposal to allow ETFs to form and operate without the need to obtain exemptive relief. This proposed rule was never adopted and there are indications that a new rule could be proposed in 2014. In March 2010, the SEC announced it would defer approval of applications for exemptive relief for ETFs that make significant use of derivatives pending a review by the SEC of the use of derivatives by mutual funds, ETFs and other investment companies. This moratorium was lifted in December 2012 and now potential competitors with the exemptive relief can compete with certain of our products. However, to date the SEC has not indicated whether the review time period or process required to obtain the initial exemptive relief will be altered. In addition, certain large mutual fund complexes have obtained exemptive relief to launch actively managed ETFs but have not done so yet. Removing the time barrier to obtain exemptive relief may bring additional competitors into the marketplace.

We believe our ability to successfully compete will depend largely on our competitive product structure and our ability to offer exposure to compelling investment strategies, develop distribution relationships, create new investment products, build trading volume and AUM in existing funds, offer a diverse platform of investment choices, build upon our successful brand and attract and retain talented sales professionals and other employees.

Regulation

The investment management industry is subject to extensive regulation and virtually all aspects of our business are subject to various federal and state laws and regulations. These laws and regulations are primarily intended to protect investment advisory clients and shareholders of registered investment companies. These laws generally grant supervisory agencies broad administrative powers, including the power to limit or restrict the conduct of our business and to impose sanctions for failure to comply with these laws and regulations. Further, such laws and regulations may provide the basis for litigation that may also result in significant costs to us.

We are currently subject to the following laws and regulations, among others. The costs of complying with such laws and regulations have increased and will continue to contribute to the costs of doing business:

| • | The Investment Advisers Act of 1940 (“Investment Advisers Act”). The SEC is the federal agency generally responsible for administering the U.S. federal securities laws. Our subsidiary, WisdomTree Asset Management, Inc. (“WTAM”), is registered as an investment adviser under the Investment Advisers Act and, as such, is regulated by the SEC. The Investment Advisers Act requires registered investment advisers to comply with numerous and broad obligations, |

13

| including, among others, recordkeeping requirements, operational procedures, registration and reporting and disclosure obligations. |

| • | The Investment Company Act of 1940. The WisdomTree ETFs are registered with the SEC pursuant to the Investment Company Act. The WisdomTree ETFs must comply with the requirements of the Investment Company Act and related regulations, as well as conditions imposed in the exemptive orders received by the ETFs, including, among others, requirements relating to operations, fees charged, sales, accounting, recordkeeping, disclosure and governance. |

| • | Broker-Dealer Regulations. Although we are not registered with the SEC as a broker-dealer under the Securities Exchange Act of 1934, as amended, nor are we a member firm of the Financial Industry Regulatory Authority (“FINRA”), many of our employees, including all of our salespersons, are licensed with FINRA and are registered as associated persons of the distributor of the WisdomTree ETFs and, as such, are subject to the regulations of FINRA that relate to licensing, continuing education requirements and sales practices. FINRA also regulates the content of our marketing and sales material. |

| • | Internal Revenue Code. WisdomTree Trust generally has obligations with respect to the qualification of the registered investment company for pass-through tax treatment under the Internal Revenue Code. |

| • | U.S. Commodity Futures Trading Commission (“CFTC”). In 2012, the CFTC adopted regulations that have required us to become a member of the National Futures Association and register as a Commodity Pool Operator for a select number of our ETFs. |

| • | Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010. This comprehensive overhaul of the financial services regulatory environment requires federal agencies to implement numerous new rules, which, as they are adopted may impose additional regulatory burdens and expenses on our business. |

Because ETFs do not fit into the regulatory provisions governing mutual funds, ETF sponsors need to obtain from the SEC exemptive relief from certain provisions of the Investment Company Act in order to operate ETFs. This exemptive relief allows the ETF sponsor to bring products to market for the specific products or structures for which the relief was requested and obtained. Applying for exemptive relief can be costly and take several months to several years depending on the type of exemptive relief sought. Each WisdomTree ETF is listed on a secondary market (each, an “Exchange”) and any new WisdomTree ETF will seek listing on an Exchange. While the SEC has already approved rules for Exchanges to allow index-based ETFs to list that meet prescribed requirements (e.g., minimum number, market value and trading volume of securities in the new ETF’s benchmark index), these rules do not allow any actively managed ETFs or index-based ETFs that do not meet the prescribed requirements without specific SEC approval. The SEC approval process has historically taken months to complete and, in some cases, years. The SEC may ultimately determine not to allow such potential new WisdomTree ETFs or may require strategy modifications prior to approval.

FINRA rules and guidance may affect how WisdomTree ETFs are sold by member firms. Although WisdomTree currently does not offer so-called leveraged ETFs, which may include within their holdings derivative instruments such as options futures or swaps, recent FINRA guidance on margin requirements and suitability determinations with respect to customers trading in leveraged ETFs may influence how member firms effect sales of certain WisdomTree ETFs, such as currency ETFs, which also use some forms of derivatives, including forward currency contracts and swaps.

Finally, our common stock is traded on the NASDAQ Global Select Market and we are therefore also subject to their rules including corporate governance listing standards. In addition, the WisdomTree ETFs are listed on NYSE Arca or the NASDAQ Market, and accordingly are subject to the listing requirements of those exchanges.

Property

Our principal executive office is located at 245 Park Avenue, New York, New York 10167. We occupy approximately 38,000 square feet of office space under a lease that expires in July 2029.

14

Intellectual Property

We regard our name, WisdomTree, as material to our business and have registered WisdomTree® as a service mark with the U.S. Patent and Trademark Office and in various foreign jurisdictions.

Our index-based equity ETFs are based on our own indexes and we do not license them from, nor do we pay licensing fees to, third parties for these indexes. We do, however, license third party indexes for certain of our fixed income, currency and alternative ETFs.

On March 6, 2012, the U.S. Patent and Trademark Office issued to us our patent on Financial Instrument Selection and Weighting System and Method, which is embodied in our dividend weighted equity indexes. We also have two patent applications pending with the U.S. Patent and Trademark office that relate to the operation of our ETFs and our index methodology. There is no assurance that patents will be issued from these applications and we currently do not rely upon our recently issued or future patents for a competitive advantage.

Employees

As of December 31, 2013, we had 87 full-time employees. Of these employees, 40 are engaged in our sales function with the remainder providing managerial, finance, marketing, legal, regulatory compliance, operations and research functions. None of our employees are covered by a collective bargaining agreement and we consider our relations with employees to be good.

Segment and Geographic Areas

We operate as one business segment, as an ETF sponsor and asset manager providing investment advisory services. Revenues are derived in the U.S. and all of our assets are currently located in the U.S.

Available Information

Company Website and Public Filings

Our website is located at www.wisdomtree.com, and our investor relations website is located at http://ir.wisdomtree.com. We make available, free of charge through our investor relations website, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q and Current Reports on Form 8-K, and amendments to those reports, filed or furnished pursuant to Sections 13(a) or Section 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after they have been electronically filed with, or furnished to, the SEC. The public may read and copy any materials filed by us with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C., 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains a website that contains reports, proxy and information statements, and other information regarding the Company at www.sec.gov.

We webcast our earnings calls and certain events we participate in or host with members of the investment community on our investor relations website. Additionally, we provide notifications of news or announcements regarding our financial performance, including SEC filings, investor events, press and earnings releases as part of our investor relations website. Further corporate governance information, including board committee charters and code of conduct, is also available on our investor relations website under the heading “Corporate Governance.” The contents of our websites are not incorporated by reference into this Annual Report on Form 10-K or in any other report or document we file with the SEC, and any references to our websites are intended to be inactive textual references only.

15

| ITEM 1A. | RISK FACTORS |

Any investment in our common stock involves a high degree of risk. You should consider carefully the specific risk factors described below in addition to the other information contained in this Report before making a decision to invest in our common stock. If any of these risks actually occur, our business, operating results, financial condition and prospects could be harmed. This could cause the trading price of our common stock to decline and a loss of all or part of your investment. Certain statements below are forward-looking statements. See the section entitled “Cautionary Note Regarding Forward-Looking Statements.”

Risks Related to Our Business and Our Industry

Recent historical growth may not provide an accurate representation of the growth we may experience in the future, which may make it difficult to evaluate our future prospects.

We launched our first 20 ETFs in June 2006. We incurred significant losses following the launch of our first ETFs. We first reported net income in the first quarter of 2011 and we only began to generate positive cash flow on a full quarterly basis in the second fiscal quarter of the year ended December 31, 2010 and, as a result, recent historical growth may not provide an accurate representation of the growth we may experience in the future, which may make it difficult to evaluate our future prospects. Although we have reported net income for the 2011, 2012 and 2013 fiscal years, we may not be able to maintain or increase our level of profitability. Prior to generating net income for 2011, we incurred net losses of $27.0 million, $21.2 million and $7.5 million in 2008, 2009 and 2010, respectively. Even though we have achieved profitability, because of the various risks outlined in this Report, we cannot assure you that we will continue to be profitable.

The significant growth we have experienced over the past three years may be difficult to sustain.

Our AUM increased from $9.9 billion as of December 31, 2010 to $34.9 billion as of December 31, 2013. The absolute measure of our AUM represents a significant rate of growth that has been and may continue to be difficult to sustain. Furthermore, as we grow larger and increase our AUM, it may become increasingly difficult to maintain our current rate of growth. In addition, as compared to 17 other traditional publicly traded asset managers, we were ranked number one for our rate of organic growth of 78.5% in 2013. The continued growth of our business will depend on, among other things, our ability to retain and recruit key investment professionals, to devote sufficient resources to maintaining existing investment strategies and to selectively develop new, value-added investment strategies. Our business growth will also depend on our success in achieving superior investment performance from our investment strategies, as well as our ability to maintain and extend our distribution capabilities, to deal with changing market conditions, to maintain adequate financial and business controls and to comply with new legal and regulatory requirements arising in response to both the increased sophistication of the investment management industry and the significant market and economic events of the last few years.

Challenging global market conditions associated with declining prices of securities can adversely affect our business by reducing the market value of the assets we manage or causing WisdomTree ETF shareholders to sell their fund shares and trigger redemptions.

We are subject to risks arising from adverse changes in global market conditions and the declining prices of securities, which may result in a decrease in demand for investment products, a higher redemption rate and/or a decline in AUM. The securities markets are highly volatile and securities prices may increase or decrease for many reasons, including general economic conditions, political events, acts of terrorism and other matters beyond our control. Substantially all of our revenue is determined by the amount of our AUM and substantially all (91%) of our AUM at December 31, 2013 was represented by equity securities, in both the international and U.S. markets. As a result, our business can be expected to generate lower revenue in declining equity market environments or general economic downturns. A decline in the prices of securities held by the WisdomTree ETFs may cause our revenue to decline by either causing the value of our AUM to decrease, which would result in lower advisory fees, or causing investors in the WisdomTree ETFs to sell their shares in favor of investments they perceive to offer greater opportunity or lower risk, thus triggering redemptions that would also result in decreased AUM and lower fees.

Fluctuations in the amount and mix of our AUM may negatively impact revenue and operating margin.

The level of our revenue depends on the level and mix of our AUM. Our revenue is derived primarily from advisory fees based on a percentage of the value of our AUM and varies with the nature of the ETFs, which have different fee levels. Fluctuations in the amount and mix of our AUM may be attributable in part to market conditions outside of our control that have had, and in the future could have, a negative impact on our revenue and operating margin.

16

We are subject to an increased risk of asset volatility from changes in the foreign markets as discussed below. Individual markets may be adversely affected by economic, political, financial, or other instabilities that are particular to the country or regions in which a market is located, including without limitation local acts of terrorism, economic crises or other business, social or political crises. Declines in these markets and currency fluctuations have caused in the past, and may cause in the future, a decline in our revenue. Changing market conditions and currency fluctuations may cause a shift in our asset mix between foreign and U.S. assets, potentially resulting in a decline in our revenue since we generally derive higher fee revenue from our ETFs investing in foreign markets, particularly in emerging markets.

We have had in the past, and in the future may have, investors who maintain significant positions in one or more of our ETFs. If such an investor were to broadly change or withdraw its investments in our ETFs because of a change to its investment strategy, market conditions or any other reason, it may significantly change the level and mix of our AUM, which may negatively affect our revenue and operating margin.

We derive a substantial portion of our revenue from a limited number of products and, as a result, our operating results are particularly exposed to the performance of those funds, investor sentiment toward the strategies pursued by those funds and our ability to maintain the assets under management of those funds.

At December 31, 2013, approximately 77% of our ETF AUM was concentrated in ten of our WisdomTree ETFs (with 35% in WisdomTree Japan Hedged Equity Fund). As a result, our operating results are particularly exposed to the performance of those funds, investor sentiment toward investing in the strategies pursued by those funds and our ability to maintain the AUM of those funds.

Most of our assets under management are held in ETFs that invest in foreign securities and we therefore have substantial exposure to foreign market conditions and are subject to currency exchange rate risks.

Many of our ETFs invest in securities of companies, governments and other organizations located outside the United States and at December 31, 2013, approximately 76% of our AUM was held by these ETFs. Therefore, the success of our business is closely tied to market conditions in foreign markets. Investments in non-U.S. issuers are affected by political, social and economic uncertainty effecting a country or region in which we are invested. In addition, fluctuations in foreign currency exchange rates could reduce the revenue we earn from these foreign invested ETFs. This occurs because an increase in the value of the U.S. dollar relative to non-U.S. currencies may result in a decrease in the dollar value of the AUM in these ETFs, which, in turn, would result in lower revenue. Furthermore, investors are likely to believe these ETFs, as well as certain of our currency and fixed income ETFs, are a less attractive investment opportunity when the value of the U.S. dollar rises relative to non-U.S. currencies, which could have the effect of reducing investments in these ETFs, thus reducing revenue.

We derive a substantial portion of our revenue from products invested in securities of Japanese companies and are exposed to the market-specific political and economic risk, as well as general investor sentiment regarding future growth of this market and currency fluctuations.

At December 31, 2013, approximately 37% of our ETF AUM was concentrated in three of our WisdomTree ETFs that primarily invest in equity securities issued by companies in Japan, including one fund, WisdomTree Japan Hedged Equity Fund, that accounted for 35% of our ETF AUM. As a result, our operating results are particularly exposed to the performance of those funds, economic and market conditions in this market, general investor sentiment regarding future growth in this market and currency fluctuations and our ability to maintain the AUM of those funds. If the AUM in these funds were to decline, either because of declining market values or because of net outflows from these funds, our revenue would be adversely affected.

17

We derive a substantial portion of our revenue from products invested in emerging markets and are exposed to the market-specific political and economic risks as well as general investor sentiment regarding future growth of those markets.

At December 31, 2013, approximately 25% of our ETF AUM was concentrated in nine of our WisdomTree ETFs that primarily invest in equity or fixed income securities issued by companies or governments in emerging markets. In 2013, approximately 41% of our revenue was derived from those nine ETFs. As a result, our operating results are particularly exposed to the performance of those funds, economic and market conditions in those emerging markets, general investor sentiment regarding future growth in those emerging markets and our ability to maintain the AUM of those funds. In addition, because these funds have a higher expense ratio than our other funds in general, they generate a disproportionate percentage of our total revenue. If the AUM in these funds were to decline, either because of declining market values or because of net outflows from these funds, our revenue would be adversely affected.

WisdomTree ETFs have a limited track record and poor investment performance could cause our revenue to decline.

Our ETFs have a limited track record upon which an evaluation of their investment performance can be made. At December 31, 2013, of our total 61 ETFs, 41 had a three year track record of which 37 ETFs had a five year track record. Furthermore, as part of our strategy, we continuously evaluate our product offerings to ensure that all of our funds are useful, compelling and differentiated investment offerings, to more competitively align our overall product line in the current ETF landscape and to reallocate our attention and resources to areas of greater client interest. As a result, we may further adjust our product offering which may result in the closing of some of our ETFs, changing their investment objective or offering of new funds. The investment performance of our funds is important to our success. While strong investment performance could stimulate sales of our ETFs, poor investment performance, on an absolute basis or as compared to third party benchmarks or competitive products, could lead to a decrease in sales or stimulate redemptions, thereby lowering the AUM and reducing our revenue. Our fundamentally-weighted equity ETFs are designed to provide the potential for better risk-adjusted investment returns over full market cycles and are best suited for investors with a longer-term investment horizon. However, the investment approach of our equity ETFs may not perform well during certain shorter periods of time during different points in the economic cycle.

We have depended upon on a third party to provide us with critical administrative services to operate our business and the WisdomTree ETFs. Commencing in April 2014, we will change to a new third party administrative provider. The failure of such administrative provider to successfully take over these services or to adequately provide such services once implemented, could materially affect our operating business and harm WisdomTree ETF shareholders.

We currently depend upon BNY Mellon to provide the WisdomTree Trust with custody services, fund accounting, administration, transfer agency and securities lending services. Commencing in April 2014, State Street Bank and Trust Company (“State Street”) will be providing these services for us. The failure of State Street to successfully provide us and the WisdomTree ETFs with these services could result in financial loss to us and WisdomTree ETF shareholders. In addition, because we have not had any experience yet with State Street and State Street will be responsible for providing a multitude of important services to us, implementing this change of providers will be challenging.

We depend on BNY Mellon and Western Asset Management to provide portfolio management services and other third parties to provide many critical services to operate our business and the WisdomTree ETFs. The failure of key vendors to adequately provide such services could materially affect our operating business and harm WisdomTree ETF shareholders.

We depend on third party vendors to provide us with many services that are critical to operating our business, including BNY Mellon and Western Asset Management, as sub-advisers that provide us with portfolio management services, third party providers of index calculation services for our indexes, a distributor of the WisdomTree ETFs and a third party provider of indicative values of the portfolios of the WisdomTree ETFs. The failure of any of these key vendors to provide us and the WisdomTree ETFs with these services could lead to operational issues and result in financial loss to us and WisdomTree ETF shareholders.

18

The asset management business is intensely competitive. Many of our competitors have greater market share, offer a broader range of products and have greater financial resources than we do. As a result, we may experience pressures on our pricing and market share.

Our business operates in intensely competitive industry segments. We compete directly with other ETF sponsors and mutual fund companies and indirectly against other investment management firms, insurance companies, banks, brokerage firms and other financial institutions that offer products that have similar features and investment objectives to those offered by us. We compete based on a number of factors, including name recognition, service, investment performance, product features and breadth of product choices, and fees. Recently several ETF sponsors with whom we directly compete are seeking to obtain market shares based on low fees. Many of our competitors have greater market share, offer a broader range of products and have greater financial resources than we do. Some financial institutions operate in a more favorable regulatory environment and/or have proprietary products and distribution channels which may provide certain competitive advantages to them and their investment products. Our competitors may also adopt products, services or strategies similar to ours, including the use of fundamentally-weighted indexes. In addition, over time certain sectors of the financial services industry have become considerably more concentrated, as financial institutions involved in a broad range of financial services have been acquired by or merged into other firms. This convergence could result in our competitors gaining greater resources and we may experience pressures on our pricing and market share as a result of these factors and as some of our competitors seek to increase market share by reducing prices. We believe that competition within the ETF industry will continue to increase as more traditional asset management companies become ETF sponsors.

Competitive pressures could reduce revenue and profit margins.

The ETF industry is becoming significantly more competitive as existing players compete on price and broaden their suite of products to different strategies, in some cases, similar to ours. Although the ETF industry currently has a higher barrier to entry as a result of the need for ETF sponsors to obtain exemptive relief from the SEC in order to operate ETFs, traditional asset managers, many of whom are much larger than us, have started to enter the ETF space. For example, in August 2013, Charles Schwab & Co. launched six ETFs using the Russell fundamentally weighted indexes with fees generally equivalent with our comparable ETFs. In September 2013, iShares filed a registration statement for three currency hedged equity ETFs including a Japan hedged equity ETF. Those ETFs launched in February 2014 with fees generally equivalent with comparable ETFs. In addition, iShares launched a floating rate treasury ETF in February 2014, on the same day as we launched our similar ETF; however, iShares waived fees for one year while we did not. Also, Deutsche Bank renamed five of their equity ETFs to stress their currency hedging strategy and launched three additional currency hedged equity ETFs. We expect that additional companies, both new and traditional asset managers, will continue to enter the ETF space.

In addition, in 2008, the SEC proposed a rule that, if adopted, would eliminate the need to obtain exemptive relief, thereby lowering the barrier to entry. This proposed rule was never adopted and there are indications that a new rule eliminating the need for exemptive relief could be proposed in 2014. In March 2010, the SEC announced it would defer approval of applications for exemptive relief for ETFs that make significant use of derivatives pending a review by the SEC of the use of derivatives by mutual funds, ETFs and other investment companies. This moratorium was lifted in December 2012 and may have served in the past to prevent potential competitors from directly competing with certain of our products. Now that the moratorium has been lifted we may face increased competition and we may be forced to compete increasingly on the basis of price, we may not be able to maintain our current fee structure. Fee reductions on existing or future new products could cause our revenue and profit margins to decline.

Our revenue could be adversely affected if the WisdomTree Trust determines that the advisory fees we receive from the WisdomTree ETFs should be reduced.

Our advisory agreements with the WisdomTree Trust and the fees we collect from the WisdomTree ETFs are subject to review and approval by the Independent Trustees of the WisdomTree Trust. The advisory agreements are subject to initial review and approval. After the initial two-year term of the agreement for each ETF, the continuation of such agreement must be reviewed and approved at least annually by a majority of the Independent Trustees. In determining whether to approve the agreements, the Independent Trustees consider factors such as (i) the nature and quality of the services provided by us, (ii) the fees charged by us and the costs and profits realized by us in connection with such services, as well as any ancillary or “fall-out” benefits from such services, (iii) the extent to which economies of scale are shared with the WisdomTree ETFs, and (iv) the level of fees paid by other similar funds. If the Independent Trustees determine that the advisory fees we charge to any particular fund are too high, we will need to reduce our fees, which could adversely affect our revenue.

19

We have contracted with a third party financial intermediary that markets our investment portfolios in Latin America and this relationship may not be available or profitable to us in the future.