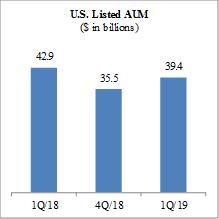

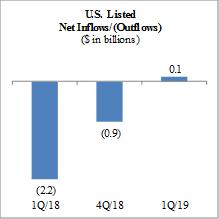

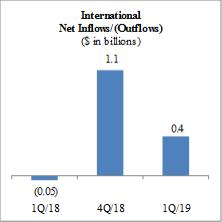

Assets Under Management

WisdomTree ETPs

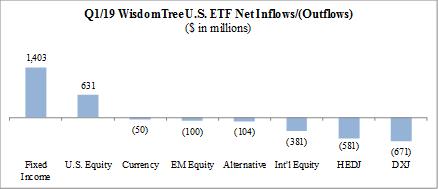

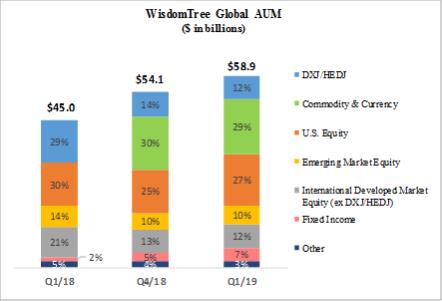

A significant portion of our AUM historically has been held in ETFs that invest in foreign securities. Therefore, our AUM and revenues are affected by movements in global capital markets and the strengthening or weakening of the U.S. dollar against other currencies. Over the last few years, concentrations in HEDJ, our European equity ETF which hedges exposure to the euro, and DXJ, our Japanese equity ETF which hedges exposure to the yen, have declined dramatically as negative investor sentiment toward these products has led to considerable net outflows. While reduced, our exposure to these two ETFs remains significant and therefore the strengthening of the euro or yen against the U.S. dollar, the decline in European or Japanese equity markets, or political or other market risks in either of these markets, may have an adverse effect on our results.

The chart below sets forth the asset mix of our ETPs at March 31, 2018, December 31, 2018 and March 31, 2019:

The ETFS Acquisition diversified our investment theme concentrations by adding commodity exposures, predominantly gold, that historically have been negatively correlated with HEDJ and DXJ. While we therefore may experience improved stability of AUM and lower overall AUM volatility, we can provide no assurance that this will be the case.

Market Environment

Performance of the U.S. and European markets recovered from prior quarter volatility as monetary policies in these markets became more accommodative and as concerns over U.S. trade policies toward China dissipated. Emerging markets posted strong returns, led by China, while the Japan markets also performed favorably although somewhat muted as compared to other markets. The price of gold, which experienced bouts of volatility, ultimately remained largely unchanged.

The S&P 500 rose 13.6%, MSCI EAFE (local currency) rose 10.7%, MSCI Emerging Markets Index (U.S. dollar) rose 12.0% and gold prices rose 1.1% during the first quarter of 2019. In addition, the European and Japan equity markets both appreciated with the MSCI EMU Index rising 9.9% and MSCI Japan Index rising 7.7%, respectively, in local currency terms for the quarter. Also, the U.S. dollar strengthened 0.5% versus the yen and 2.0% versus the euro during the quarter.

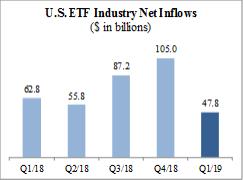

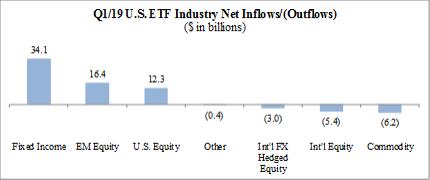

U.S. Listed ETF Industry Flows

As the charts below reflect, U.S. listed ETF net flows for the three months ended March 31, 2019 were $47.8 billion. Fixed income, emerging market equity and U.S. equity gathered the majority of those flows.

34